How to Get a Car Insurance Discount

Most drivers pay more for insurance than they need to. An auto insurance discount rarely comes from a single factor – the drivers who pay significantly less than average typically qualify through a combination of record history, course completions, and policy choices. Knowing how to get a discount on auto insurance starts with understanding that insurers use dozens of rating variables, and two drivers with identical vehicles and zip codes can pay substantially different premiums based on what is on their records. An auto insurance discount is not automatic – it requires knowing which conditions trigger it and acting on them.

What Affects Your Auto Insurance Premium

Insurers calculate premiums from two types of factors: fixed ones like age, location, and vehicle type, and variable ones like driving record, claims history, and course completions. Fixed factors cannot be changed. The variable ones can – and that is where most auto insurance discount opportunities sit.

A single at-fault accident raises premiums by 20-40% and typically stays on the policy for three to five years. A moving violation adds a smaller surcharge but compounds if a second citation follows within the same rating window. Conversely, a clean three-year period after a violation gradually restores standard rates as the incident ages off the record.

Claims history works the same way. A driver who files multiple small claims over a short period may pay more than one who absorbs minor costs out of pocket and keeps the claims record clean.

How to Get a Discount on Auto Insurance

A discount on auto insurance comes from three distinct categories – driving behavior, course completion, and policy structure. Most drivers qualify for at least one without realizing it.

Discounts for Safe Driving and Clean Records

The most common car insurance discount is the good driver discount – typically 10-25% off for drivers with no at-fault accidents or violations in the past three to five years. The exact threshold varies by insurer. Telematics programs offer a separate route: the insurer installs an app or device that tracks real driving behavior, and the discount reflects actual habits rather than historical record.

Discounts for Course Completion

Completing a state-approved driving course qualifies drivers for a discount for auto insurance in most states, applied at the next renewal after the certificate is submitted to the insurer. The discount range is typically 5-15%, depending on the state and provider. In some states the reduction is mandated by law – insurers are required to apply it. In others it is discretionary, meaning the driver should confirm with their insurer before enrolling.

ETS offers state-approved courses specifically designed for insurance savings, including mature driver improvement and insurance discount programs. An Insurance Discount Course is available across multiple states – 100% online, self-paced, with the completion certificate delivered upon finishing.

Vehicle, Policy, and Payment Discounts

Discounts unrelated to driving behavior are often the most overlooked. Bundling home and auto insurance with the same insurer typically saves 10-20% on the auto portion. Vehicles with anti-lock brakes, airbags, and anti-theft systems qualify for safety feature discounts at most major insurers. Paying the full annual premium upfront – rather than monthly – removes the installment fee and reduces the effective rate.

Insurance Discount Driving Course: How It Works

An insurance discount driving course is a state-approved program that triggers a premium reduction when the completion certificate is submitted to the insurer. The course itself does not contact the insurer – the driver submits the certificate, and the discount applies at the next renewal cycle.

What Is a Car Insurance Discount Course

A car insurance discount course is a defensive driving or mature driver improvement program reviewed and approved by the state before it qualifies for any insurance benefit. The approval status determines whether the insurer is required to apply the discount or can decline it.

In states where the discount is mandated by law, insurers must offer the reduction after a qualifying course completion regardless of the driver's prior record. In states where it is discretionary, the insurer sets its own eligibility conditions. Delaware offers a state-approved 6-hour Insurance Discount Course at $16.00 – one of the lowest-cost options available. For drivers 55 and older, mature driver improvement courses qualify for a mandatory discount in several states under specific insurance code provisions.

When a Defensive Driving Course May Help

A car insurance discount defensive driving course is most effective when a driver has recent violations that raised premiums. Completing a course can offset part of the surcharge in states where the discount is mandated – the reduction applies on top of the existing rate, not as a replacement for the violation surcharge.

In several states, the mandated discount runs for three years from the date the certificate is submitted. Timing the completion close to renewal maximizes the benefit across the full discount period.

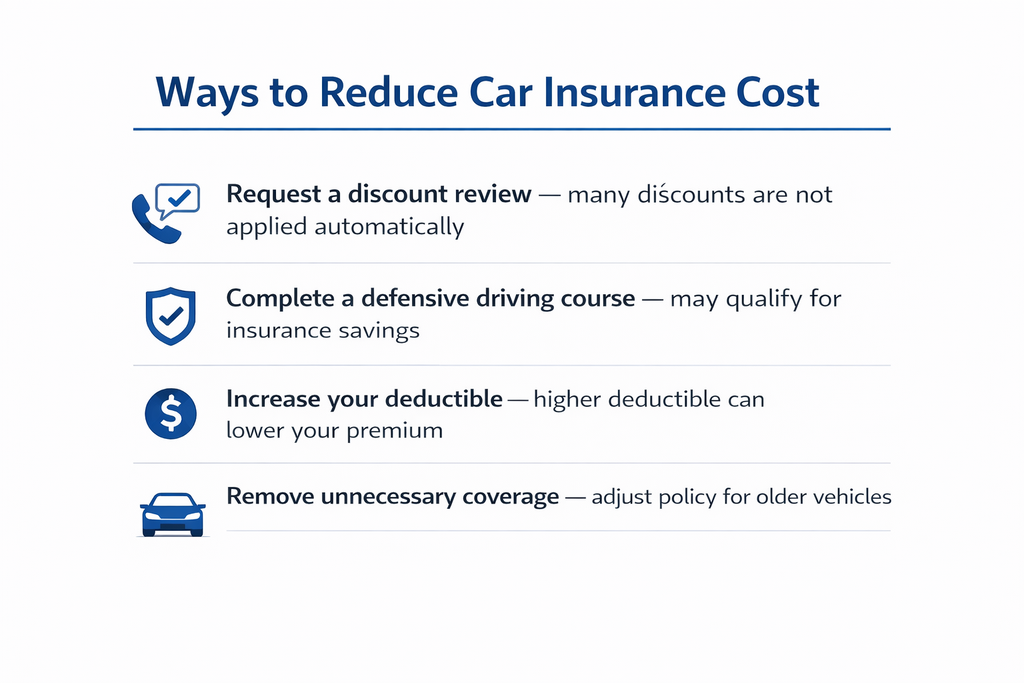

Ways to Reduce Car Insurance Cost Without Changing Insurers

ways to reduce car insurance cost

The most direct ways to reduce car insurance cost do not require switching providers – they require asking the right questions and adjusting the existing policy.

Most drivers never request a discount review. Insurers are not required to proactively notify policyholders of available discounts, which means a driver who qualifies for a good driver discount, a course completion discount, and a safety feature discount may be paying full rate simply because no one asked. A single call or online policy review can surface discounts that have been sitting unclaimed for years.

Raising the deductible is another lever. Moving from $500 to $1,000 typically reduces the premium by 10-20%, depending on the insurer. The tradeoff is higher out-of-pocket cost after a claim – but for drivers with clean records and low claim frequency, the annual savings often outweigh the risk.

Among other ways to save on auto insurance, removing comprehensive and collision coverage on older vehicles where the combined annual cost exceeds the vehicle's market value is a straightforward adjustment that many drivers delay longer than necessary.

How to Lower Your Car Insurance Premium Over Time

Knowing how to lower car insurance premium over multiple years requires a consistent approach rather than a single action. The drivers who see the largest reductions over time combine clean record maintenance with periodic policy reviews and course completions timed to renewal cycles.

Three consecutive violation-free years typically restores standard rates after a surcharge – but only if the driver requests a review. Insurers recalculate at renewal using the current record, but they do not always volunteer the adjustment. A driver who cleared a violation three years ago may still be paying the surcharge rate without realizing it.

Course completions reset the insurance benefit clock. The discount period runs from the date the certificate is submitted – a driver who completes a course six months before renewal gets six months of benefit before the next cycle. Completing it closer to renewal maximizes the full discount period.

Adding a young driver to a policy raises rates by 50-100% at most insurers. A completed driver education course for that driver reduces the surcharge – the reduction varies by insurer but is available at most major providers.

Common Mistakes That Keep Drivers From Getting Discounts

Most missed discounts result from inaction rather than ineligibility.

Not submitting the course completion certificate to the insurer is the most common one. The discount does not apply automatically – the driver is responsible for delivering the certificate, and the insurer applies the reduction only after receiving it. ETS submits the completion certificate to the court or DMV automatically, but the insurance discount step requires the driver to contact their insurer directly.

Assuming the discount was applied without confirming it is a related mistake. A driver who completed a course, submitted the certificate, and never followed up may have had the request processed incorrectly or applied to the wrong policy period.

Waiting until renewal to address a violation surcharge misses a potential mid-term adjustment. Some insurers allow rate recalculations before the renewal date if the record has changed – a driver who completed a course or had a violation age off the record mid-term can request a review rather than waiting months for the next cycle.

Not comparing rates after a clean record period is the fourth. Loyalty to an insurer does not guarantee the best available rate. A driver with three clean years who has never shopped competing quotes may be paying significantly more than the market rate for their current record.

Conclusion

An auto insurance discount works best as a combination – clean record, course completion, and policy optimization each contribute independently and can stack. No single action produces the maximum reduction on its own. The drivers who pay the least over time are the ones who maintain their record, submit course certificates on time, review their policy annually, and ask their insurer what they qualify for.

ETS offers state-approved courses including insurance discount and mature driver improvement programs – 100% online, self-paced, available across all 50 states, with completion certificates delivered upon finishing.

FAQs

Can you combine several auto insurance discounts at the same time?

Yes. Most insurers allow multiple discounts to stack on the same policy – good driver, course completion, bundling, and safety feature discounts can all apply simultaneously. The total reduction depends on the insurer's stacking rules, but combining discounts is one of the most effective ways to lower the overall premium.

Will a discount still apply if you switch insurance companies?

Not automatically. Discounts are insurer-specific – a good driver discount or course completion benefit does not transfer when switching providers. The new insurer will assess eligibility based on the driving record and any certificates submitted at the time of the new policy application.

Do all insurers offer the same discount for completing a driving course?

No. In states where the discount is mandated by law, insurers must apply a set reduction. In states where it is discretionary, the amount and eligibility conditions vary by provider. Drivers should confirm the discount amount and submission requirements with their insurer before enrolling in a course.

Can a higher deductible help lower your premium enough to matter?

Yes. Raising the deductible from $500 to $1,000 typically reduces the premium by 10–20% depending on the insurer and coverage type. The tradeoff is higher out-of-pocket cost after a claim – the adjustment works best for drivers with clean records and low claim frequency.

Is it better to ask for discounts before or after renewing your policy?

Before. Requesting a discount review before the renewal date gives the insurer time to apply adjustments to the upcoming cycle. Asking after renewal may delay the benefit until the next cycle. Drivers who completed a course or maintained a clean record mid-term should contact their insurer before the renewal date to maximize the timing.